Many African governments have had to weigh up the difficult decision between facing a humanitarian crisis or an economic one as COVID-19 infections hit the continent. While countries such as Rwanda and South Africa have been lauded for their rapid and wide-reaching lockdown response to the pandemic, public pressure to ease COVID-19 restrictions is now mounting amid the worsening economic consequences of the crisis. International institutions and regional think tanks are warning of the severe economic challenges that will affect much of Africa in 2020 and their concerns are not misplaced.

According to the UN Economic Commission for Africa, in the best case scenario, Africa’s GDP for 2020 will fall from 3.2 percent to 1.8 percent; in the worst case, the economy could contract by 2.6 percent as a result of the pandemic. This would push a further 29 million people into poverty. To compound matters, Africa is also increasingly debt distressed, and while international bodies such as the International Monetary Fund and World Bank are discussing debt relief, China’s Export Import Bank, for example, has yet to show the same commitment. This is particularly concerning as, according to John Hopkins School of Advanced International Relations’ China Africa Research Initiative, around 20 percent of all African government debt is owed to China. The combined impact of COVID-19, government responses to the outbreak and the wider global economic consequences will be particularly acute in Africa. The sharp fall in oil prices has heavily impacted the region’s oil-exporting economies, including Angola, Nigeria, Gabon and Equatorial Guinea, while other economies have been impacted by price fluctuations in other commodities. Weak external demand, disruptions to supply chains and reduced domestic production will curb economic growth. Furthermore, the collapse of the informal sector, which employs 66 percent of Africa’s workforce, will place significant social and financial burdens on governments and relief operations.

But while managing the economic fallout is paramount, many African countries will also be faced with increasingly complex political and security environments, which will become progressively volatile in the post-COVID-19 context.

The Numbers

|

+ 29 million people pushed into poverty |

Africa’s economy could contract by 2.6% |

| 20% of all African government debt is owed to China | 66% of Africa’s workforce is employed in the informal sector |

Big men and big elections

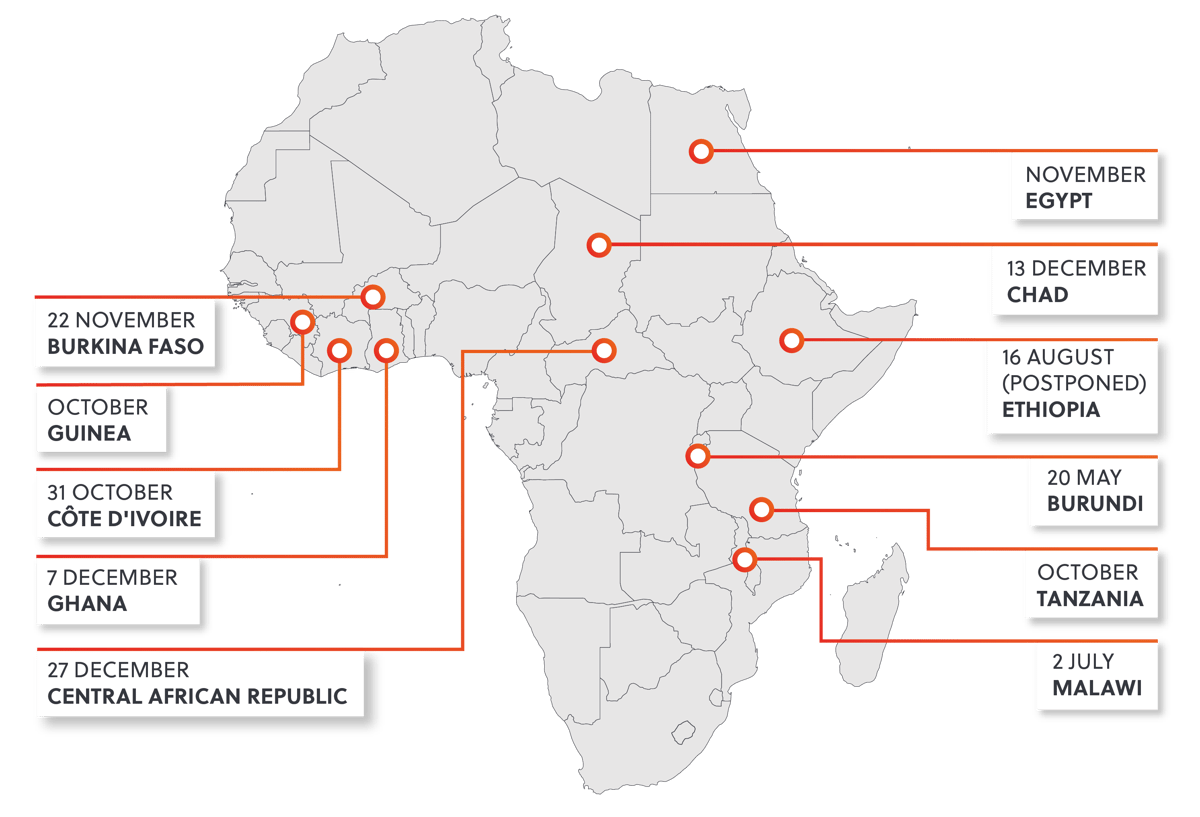

2020 was already set to be a big election year in Africa with votes scheduled in Cote d’Ivoire, Ghana, Guinea, Tanzania and several others. These upcoming elections could face serious legitimacy challenges should restrictions lead to low voter turnouts or if any COVID-19 related election postponements are seen as politically motivated. Public tensions are already high in certain jurisdictions and the potential for election-related unrest is rising while turbulent elections will create unique uncertainties in the business environment. According to Andrew Munro, the Managing Director of specialist insurance underwriter, Praesidio Risk Managers, the pandemic will not necessarily result in new challenges for operating in Africa, but rather significantly exacerbate the impact and frequency of current political challenges.

The potential for election-related unrest is rising while turbulent elections will create unique uncertainties in the business environment.

Commentators are warning that some leaders could use the pandemic as a convenient conduit to push through more authoritarian style policies. Uganda’s President Yoweri Museveni, for example, ensured that opposition politicians could not shore up support during the crisis, banning opposition parties from distributing relief packages. Meanwhile, Malawian President Peter Mutharika’s early call to ban gatherings of more than 100 people served a dual purpose in quelling protests against the disputed 2019 elections. The election rerun for the annulled ballot was scheduled for July 2020 but will likely be delayed. Other leaders could also look to postpone important ballots in response to the pandemic. Ethiopia has already postponed their August 2020 general elections due to the pandemic but while the move was welcomed by health experts, it is uncertain whether reformist Prime Minister Abiy Ahmed will be able to appease worsening ethno-political divisions in the country.

In Guinea, President Alpha Condé pushed through with March 2020 legislative elections and a constitutional referendum, which will pave the way for him to secure another term in the October presidential vote. This was despite widespread unrest denouncing the referendum during the March vote which resulted in the death of at least 32 people. Although unrest died down amid COVID-19 restrictions, tensions are still simmering and the run up to the presidential election is likely to be marred by unrest for this major Bauxite and alumina producer. With President Condé likely to employ all means necessary to stay in office, there will be little improvement in Guinea’s commercial space, currently inhibited by weak rule of law, and political interference.

The October elections in Cote d’Ivoire could prove more challenging. Although President Alassane Ouattara has said he will not seek a controversial third term, instead backing prime minister, Amadou Gon Coulibaly, the election is expected to be highly competitive. Amid fears of a repeat of the 2010/2011 political conflict and as political alliances which have underpinned economic growth falter, the global cocoa producer’s economic trajectory is also at stake. Though a rerun of the 2010/2011 crisis appears unlikely at this stage, several factors increase the probability of a turbulent election. Among these are regional and identity-based divisions, an incomplete disarmament programme and other legacies of the 2010/2011 conflict, including a spate of military mutinies in 2018.

Ghana is perhaps an exception. The government’s response in Ghana is widely seen as a test of the current administration under President Nana Akufo-Addo of the New Patriotic Party (NPP). If the administration manages the COVID-19 crisis well and navigates Ghana through the immediate aftermath effectively, President Akufo-Addo and the NPP will be in a good position to secure another term in the December 2020 elections. However, NPP and opposition party, National Democratic Congress (NDC)’s election primaries and voter registration could still be inhibited by COVID-19. Furthermore, a recent dispute over new software onboarded by the Electoral Commission will provide avenues for losing parties to question the election results and drum up possible protests.

But public frustrations and anti-government sentiments will not only play out on the street and through the ballot box. Non-state actors are also likely to seek to capitalise on distracted governments.

AFRICA ELECTION MAP: 2020

Guns unsilenced

2020 marks the final year of the African Union’s ‘Silencing the Guns’ campaign, aimed at “ending all wars, civil conflicts, gender-based violence, violent conflicts and preventing genocide in the continent by 2020.” Yet, at the start of the year, findings from research houses such as the Armed Conflict Location & Event Data Project (ACLED) and humanitarian organisations like the International Committee of the Red Cross (ICRC) painted a different picture. During a press conference in South Africa in early 2020, Patricia Danzi, Regional Director for Africa for the ICRC claimed that while aid agencies are already under strain due to conflicts, new crises keep emerging. This situation has worsened under COVID-19 restrictions.

Although the medium to longer term impact of COVID-19 on security in Africa will be difficult to determine, there is consensus among global and regional institutions, think tanks and humanitarian agencies that the pandemic will add new stress to governance systems already faltering under pressure from conflict and violence extremism.

Non-state actors are likely to use the socio-economic fallout from COVID-19 to capitalise on anti-government sentiments, shoring up support within vulnerable communities, or using the distraction of security forces to step up their campaigns. In Somalia, Islamist militant group Al Shabaab has adopted a different strategy, dismissing the pandemic, claiming the disease was “spread by the crusader forces”, referring to the West, and calling for further attacks. Although the group has not carried out any mass casualty bombings over April / May, it has maintained constant attacks against Somali and interventionary security forces undisrupted. Leader of Boko Haram faction, Abubakar Shekau has taken a similar approach in Nigeria’s Borno State, where violence continues amid his dismissal of government response measures. Meanwhile, the need to restrict travel and close borders to curb the spread of the virus has in turn impacted the movement of peacekeepers in the region, facilitating increased terrorist attacks in the Sahel and the Lake Chad Basin.

Emboldened armed groups could be encouraged to attack larger commercial targets, particularly those operating in remote areas

Through the stagnation of peace processes and the redirection of security forces to enforce the lockdown measures, non-state groups could exploit security vulnerabilities in the coming months. Continuing conflicts and terror campaigns already present a threat to the safety of personnel and products along distribution routes, but emboldened armed groups could be encouraged to attack larger commercial targets, particularly those operating in remote areas such as the extractive sector.

2020 and beyond

2020 will be difficult for many African governments as well as potential investors as they navigate the inevitable economic, political and security challenges that lie ahead. Although lower than expected COVID-19 cases on the continent have brought some reprieve to investors, the longer-term ramifications of lockdowns, intertwined with the status of the global economy, could present hurdles for countries easing restrictions and resuming economic activity.

Commercial operators in new and old markets will be presented with unique challenges given altered operating environments, where the viability and means of investment will need to be reassessed.

While many governments will be eager to offset the economic fallout of COVID-19 through FDI and therefore ease entry into their markets, social pressures may result in increased local content regulations and / or community engagement prerequisites for investors. From the perspective of the insurance sector, Munro cautioned that businesses will need to adapt their risk management protocols and strategy to take into account heightened risks of unrest and criminal activity. Furthermore, with conflicts likely to have evolved during the COVID-19 pandemic, we could see resultant security threats move closer to the commercial space. With this in mind, commercial operators in new and old markets will be presented with unique challenges given altered operating environments, where the viability and means of investment will need to be reassessed.

Yet, should certain African jurisdictions effectively steer their economic reopening while keeping the number of COVID-19 cases in check, this could present new opportunity in Africa. Having responded to the pandemic with the advantage of hindsight, monitoring conditions seen elsewhere in China and Europe, the balance of short-term economic shutdowns against a health crisis could still pay off. Although a return to ‘business as usual’ is less likely, investors willing to reassess positions in Africa may find unique openings in the African market.

Email Gabrielle

Email Gabrielle

@SRMInform

@SRMInform

S-RM

S-RM

hello@s-rminform.com

hello@s-rminform.com